Income statement reports show financial performance based on revenues, expenses, and net income. By regularly analyzing your income statements, you can gather key financial insights about your company, such as areas for improvement or projections for future performance.

Learn how your business can create and use income statements, along with other financial statements.

The income statement, also known as a profit and loss statement , shows a business’s financial performance during a specific accounting period. It reports net income by detailing a business’s revenues, gains, expenses, and losses. Put simply, an income statement follows this equation:

Total revenue – total expenses = net income

The income statement serves as a tool to understand the profitability of your business. The income statement can also help you make decisions about your spending and overall management of business operations. Income statements should be generated quarterly and annually to provide visibility throughout the year.

The information gleaned from the income statement can help you:

The income statement should be used in tandem with the balance sheet and cash flow statement . With insights from all three of these financial reports, you can make informed decisions about how best to grow your business.

An income statement provides a clear picture of your business’s financial position. There are several ways to use periodically generated income statements to more efficiently manage your business.

By generating income statements and other financial reports on a regular basis, you can analyze the statements over time to see whether your business is turning a profit. You can use this information to make financial projections and more informed decisions about your business.

Understanding cash flow is critical for small businesses. When used in conjunction with the other financial statements, an income statement can give you a clear view of your cash flow.

Many small businesses need financial statements to apply for credit or to provide financial information to a potential lender. Using an income statement to demonstrate a consistent history of income and profitability can make this process easier.

Accurate records of expenses, revenues, and credits are required for tax purposes and can help keep you in compliance with tax regulations.

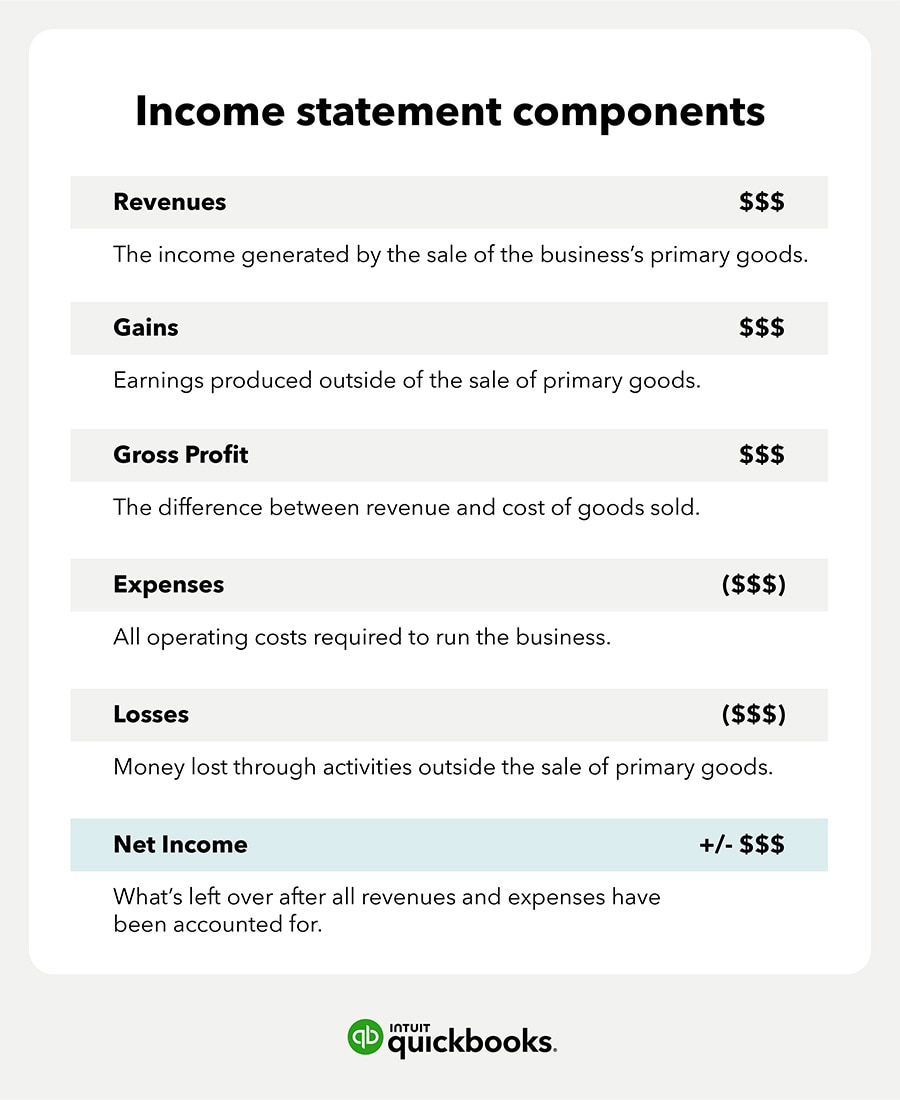

Components of an income statementThe elements of an income statement include revenues, gains, gross profit, expenses, losses, and net income or loss.

Revenue is all income generated by the sale of the business’ primary goods or services. Revenue may also be referred to as the “top line,” because it is the first line on the income statement.

Gains are the earnings produced outside of the sale of your main goods or services. For example, selling off an asset can be categorized under gains.

Gross profit is what's left of your revenue after deducting the cost of goods sold (COGS)—the direct costs related to producing goods or providing services.

Revenue – COGS = gross profit

Expenses include all operating expenses required to run your business. Operating expenses —also known as selling, general, and administrative expenses—include costs such as advertising, insurance, and rent. The costs associated with producing your goods or providing services are not included in the expenses section of the income statement.

Losses include money lost through activities outside of transactions for your primary goods or services. For example, paying out a lawsuit settlement is considered a loss.

Net income—or loss—is what is left over after all revenues and expenses have been accounted for. If there is a positive sum (revenue was greater than expenses), it’s referred to as net income. If there’s a negative sum (expenses were greater than revenue during that period), then it’s referred to as net loss.

Net income = (total revenue + gains) – (total expenses + losses)

Preparing financial statements can seem intimidating, but it doesn’t have to be an overwhelming process. We’ve broken down the steps for preparing an income statement, as well as some helpful tips.

Income statements can be prepared monthly, quarterly, or annually, depending on your reporting needs. Larger businesses typically run quarterly reporting, while small businesses may benefit from monthly reporting to better track business trends.

A balance report details your end balance for each account that will be listed on the income statement. This can be done with accounting software, like QuickBooks Online . A balance report provides all of the end balances required to create your income statement.

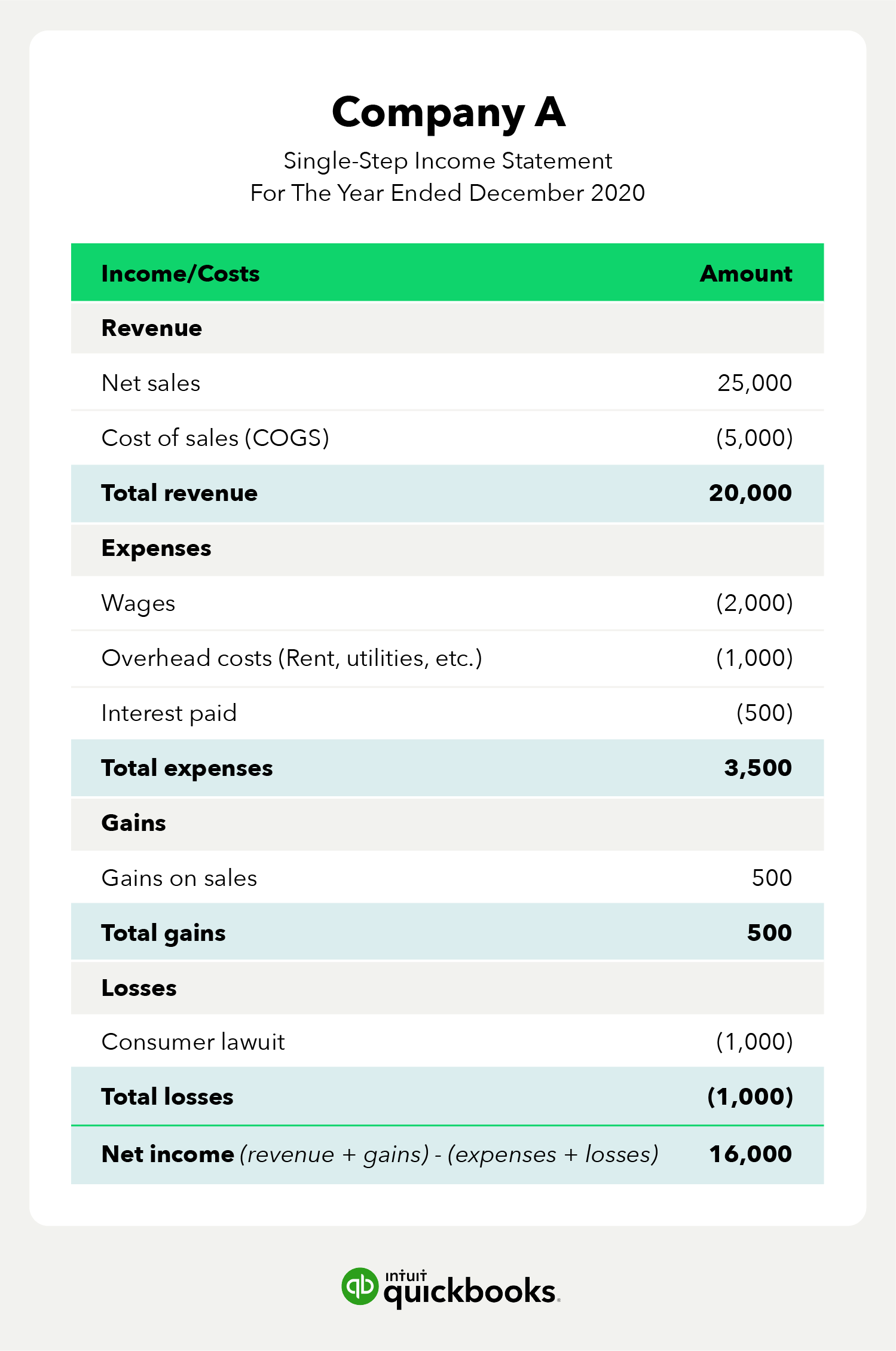

Single-step income statements can be used to get a simple view of your business’s net income. These take minimal time to prepare and don't differentiate operating versus non-operating costs.

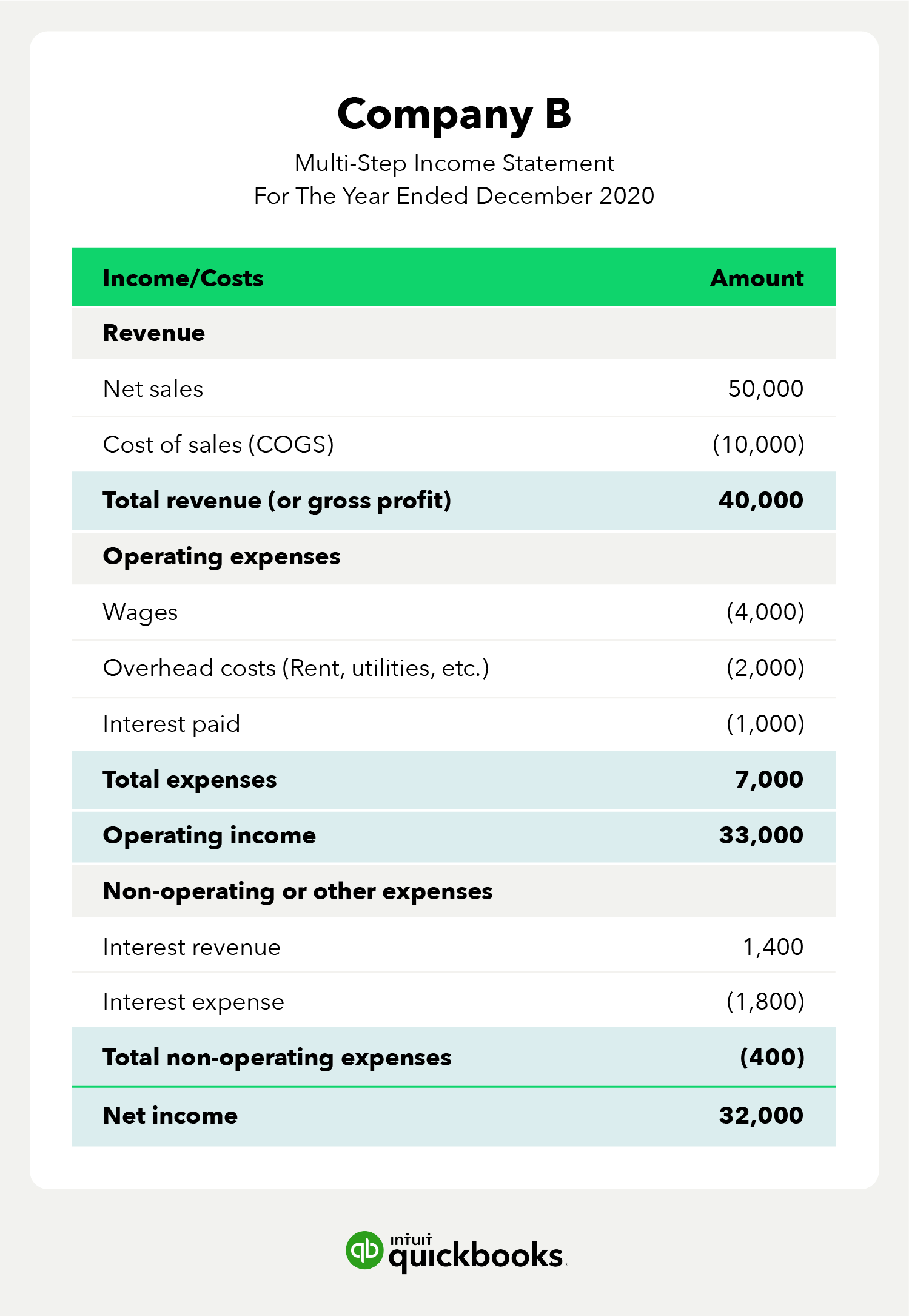

A multi-step income statement calculates net income and separates operational income from non-operational income—giving you a more complete picture of where your business stands.

Jump to find more details and examples of these two types of income statements:

Give your statement a final QA either manually or using an automated platform. Using software allows you to automatically track and organize your business’s accounting data so you can access and review income statements.

You can use QuickBooks Live to get help generating income statements and other key financial reports.* You can also download our free income statement template to streamline the process or partner with a live bookkeeper to help you understand your company’s finances.*

When deciding how you’d like to report your net income, it’s important to consider the pros and cons of both single-step and multi-step income statements.

Single-step income statements are the simplest and most commonly used by small businesses. But multi-step income statements are great for small businesses with several income streams.

For small businesses with few income streams, you might generate single-step income statements on a regular basis and a multi-step income statement annually. If you have more than a few income streams or a complicated financial landscape, you might use multi-step income statements to get a better view of your profits and losses.

Typically, multi-step income statements are used by larger businesses with more complex finances. This is because they provide greater detail. However, multi-step income statements can benefit small businesses that have a variety of revenue streams. There are several ways multi-step income statements can benefit your small business.

A single-step income statement is a simplified approach to viewing your net profit or loss. Single-step income statements include revenue, gains, expenses, and losses, and they strictly show operating costs.

For single-step income statements, you need only one calculation: net income. To determine net income, you simply subtract all your expenses from total revenue.

Net income = (revenues + gains) – (expenses + losses)

A multi-step income statement uses a more complex method of calculating net profit or loss. Multi-step income statements add in four measures of profitability: gross, operating, post-tax, and pre-tax, and they use separate operating and non-operating expenses. This gives a more detailed financial picture.

For the multi-step income statement method, you need to complete three additional steps:

1. Find gross profit

Gross profit = net sales – COGS

2. Find operating income

Operating income = gross profit – operating expense

3. Calculate net income

Net income = operating income + non-operating income

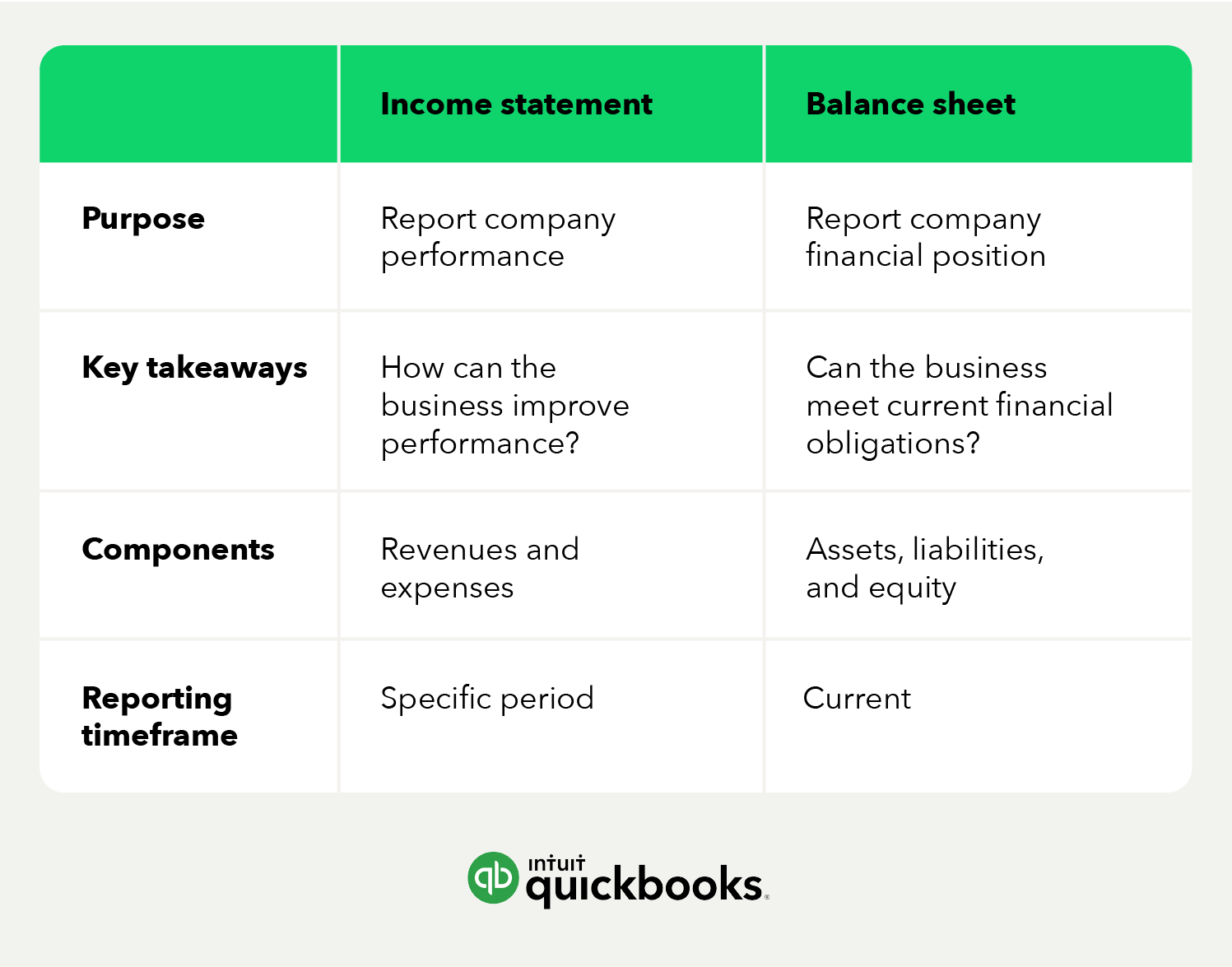

The income statement and balance sheet are two of the main financial statements businesses use, in addition to the cash flow statement. But they have key differences, which include:

looking at their purpose, components, and reporting timeframe." width="" />

looking at their purpose, components, and reporting timeframe." width="" />

An income statement is a valuable tool for guiding your business’s financial decisions. While you can prepare income statements on your own, accounting software can help provide simplicity and accuracy. With QuickBooks Live ,* you can work with accounting experts to keep tabs on your financial standing, while spending less time crunching numbers and more time building your business.

*QuickBooks Live Bookkeeping requires QuickBooks Online subscription. Additional terms, conditions, limitations, and fees apply.

Recommended for you

How to read and prepare a balance sheet

Understanding the critical differences between profit and cash flow

How to measure profitability: 3 surefire strategies

We provide third-party links as a convenience and for informational purposes only. Intuit does not endorse or approve these products and services, or the opinions of these corporations or organizations or individuals. Intuit accepts no responsibility for the accuracy, legality, or content on these sites.

**Product information

QuickBooks Live Assisted Bookkeeping: This is a monthly subscription service offering ongoing guidance on how to manage your books that you maintain full ownership and control. When you request a session with a Live Bookkeeper, they can provide guidance on topics including: bookkeeping automation, categorization, financial reports and dashboards, reconciliation, and workflow creation and management. They can also answer specific questions related to your books and your business. Some basic bookkeeping services may not be included and will be determined by your Live Bookkeeper. The Live Bookkeeper will provide help based on the information you provide.

QuickBooks Live Full-Service Bookkeeping: This is a combination service that includes QuickBooks Live Cleanup and QuickBooks Live Monthly Bookkeeping.

1. QuickBooks Online Advanced supports the upload of 1000 transaction lines for invoices at one time. 37% faster based off of internal tests comparing QuickBooks Online regular invoice workflow with QuickBooks Online Advanced multiple invoice workflow.

2. Access to Priority Circle and its benefits are available only to customers located in the 50 United States, including DC, who have an active, paid subscription to QuickBooks Desktop Enterprise or QuickBooks Online Advanced. Eligibility criteria may apply to certain products. When customers no longer have an active, paid subscription, they will not be eligible to receive benefits. Phone and messaging premium support is available 24/7. Support hours exclude occasional downtime due to system and server maintenance, company events, observed U.S. holidays and events beyond our control. Intuit reserves the right to change these hours without notice. Terms, conditions, pricing, service, support options, and support team members are subject to change without notice.

3. For hours of support and how to contact support, click here.

4. With our Tax Penalty Protection: If you receive a tax notice and send it to us within 15-days of the tax notice we will cover the payroll tax penalty, up to $25,000. Additional conditions and restrictions apply. See more information about the guarantee here: https://payroll.intuit.com/disclosure/.

Terms, conditions, pricing, special features, and service and support options subject to change without notice.

QuickBooks Payments: QuickBooks Payments account subject to eligibility criteria, credit, and application approval. Subscription to QuickBooks Online required. Money movement services are provided by Intuit Payments Inc., licensed as a Money Transmitter by the New York State Department of Financial Services. For more information about Intuit Payments' money transmission licenses, please visit https://www.intuit.com/legal/licenses/payment-licenses/.

QuickBooks Money: QuickBooks Money is a standalone Intuit offering that includes QuickBooks Payments and QuickBooks Checking. Intuit accounts are subject to eligibility criteria, credit, and application approval. Banking services provided by and the QuickBooks Visa® Debit Card is issued by Green Dot Bank, Member FDIC, pursuant to license from Visa U.S.A., Inc. Visa is a registered trademark of Visa International Service Association. QuickBooks Money Deposit Account Agreement applies. Banking services and debit card opening are subject to identity verification and approval by Green Dot Bank. Money movement services are provided by Intuit Payments Inc., licensed as a Money Transmitter by the New York State Department of Financial Services.

QuickBooks Commerce Integration: QuickBooks Online and QuickBooks Commerce sold separately. Integration available.

QuickBooks Live Bookkeeping Guided Setup: The QuickBooks Live Bookkeeping Guided Setup is a one-time virtual session with a QuickBooks expert. It’s available to new QuickBooks Online monthly subscribers who are within the first 30 days of their subscription. The QuickBooks Live Bookkeeping Guided Setup service includes: providing the customer with instructions on how to set up chart of accounts; customized invoices and setup reminders; connecting bank accounts and credit cards. The QuickBooks Live Bookkeeping Guided Setup is not available for QuickBooks trial and QuickBooks Self Employed offerings, and does not include desktop migration, Payroll setup or services. Your expert will only guide the process of setting up a QuickBooks Online account. Terms, conditions, pricing, special features, and service and support options subject to change without notice.